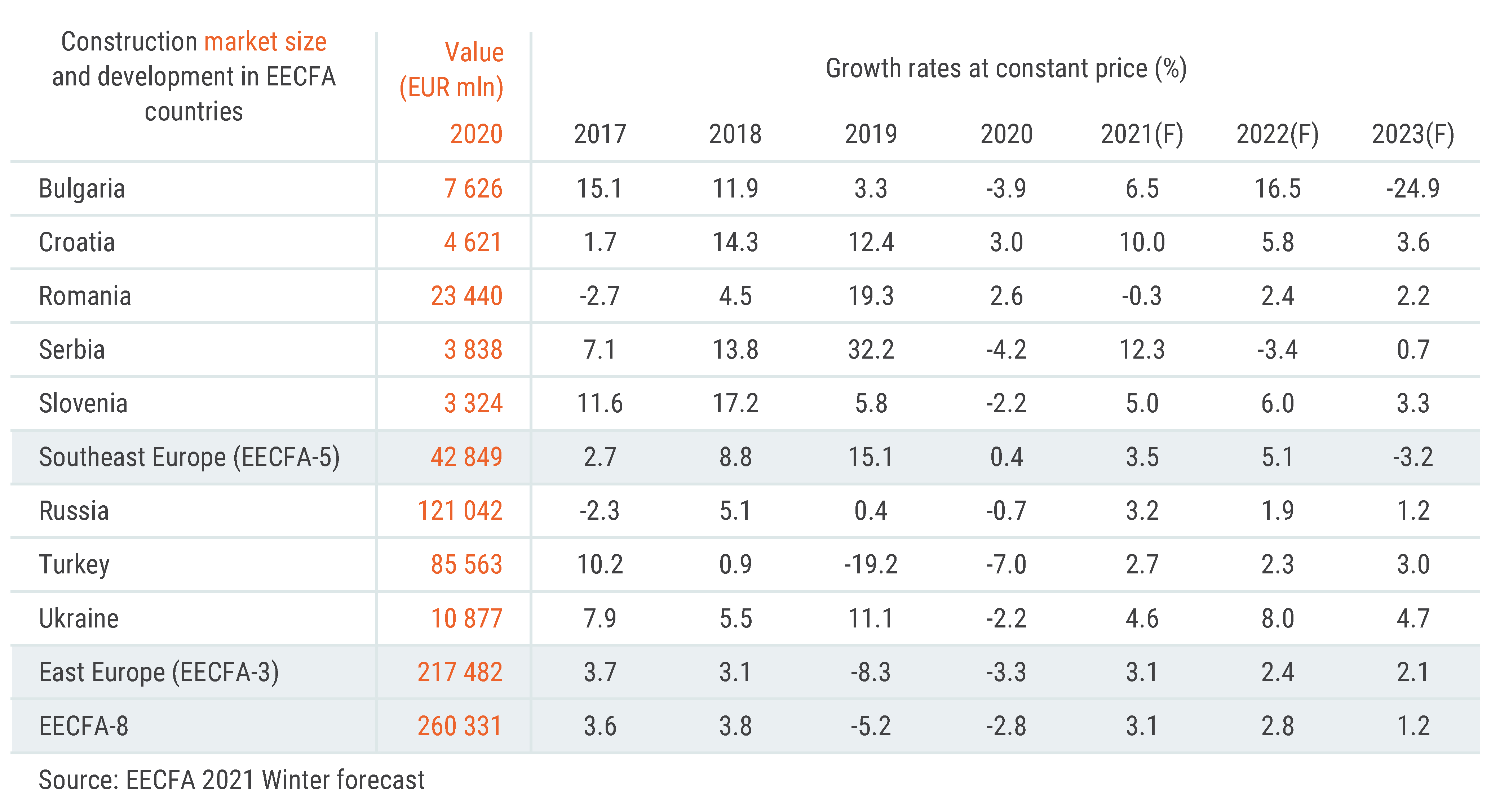

EECFA’s 2021 Winter Construction Forecast Report was released on 6 December. EECFA (Eastern European Construction Forecasting Association) conducts research on the construction markets of 8 Eastern-European countries.

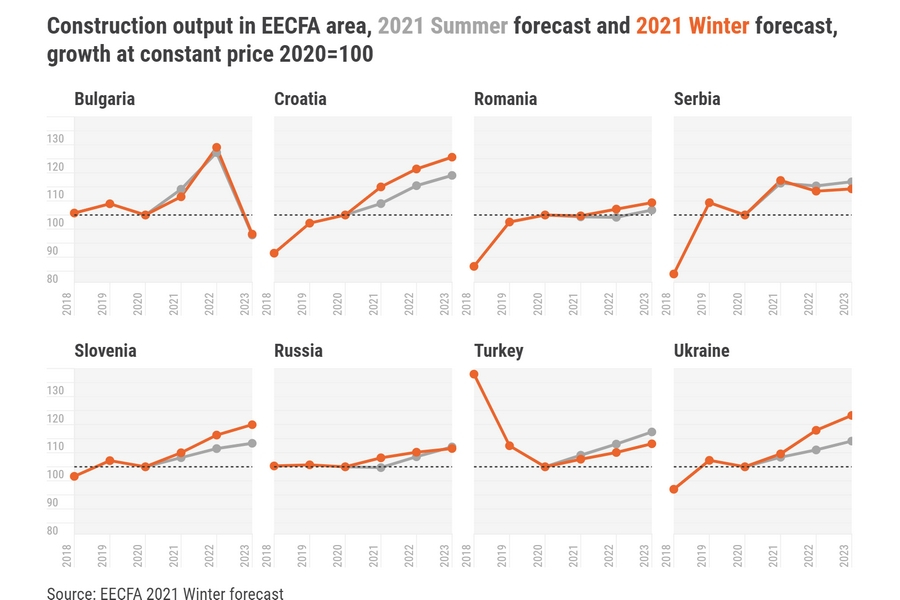

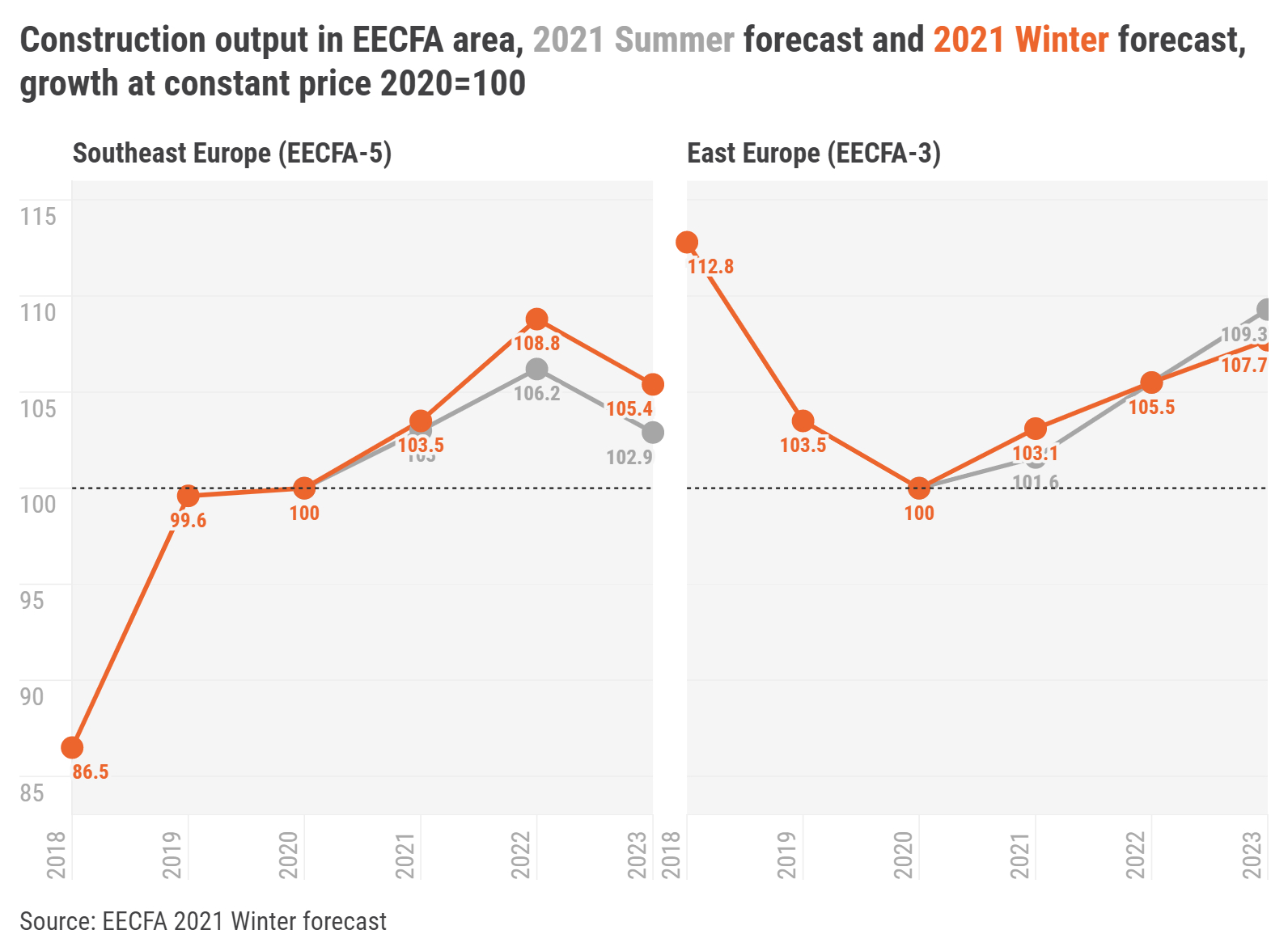

We are more optimistic for 2022 in the Southeast European region of EECFA than in the previous forecast round. The drop in 2023 is caused by Bulgaria; the awaited shrinkage is so sizeable there that expansion elsewhere in the region might not counterbalance it. Expansion in the East European region of EECFA is foreseen to be smaller both in 2022 and in 2023 than in the previous forecast round. Growth in Turkey was revised downward.

The largest Southeast European construction market of EECFA, Romania, is expected to see only moderate growth on the horizon. Serbia, having recorded the biggest expansion of almost 100% in the 2014-2020 period, is foreseen to plateau in the upcoming years. In Eastern Europe, in Turkey we maintain to believe that the recovery could start, but we lowered our growth expectation compared to our previous forecast. After 2 years of no-growth, Russia's construction market is foreseen to expand gradually until 2023.

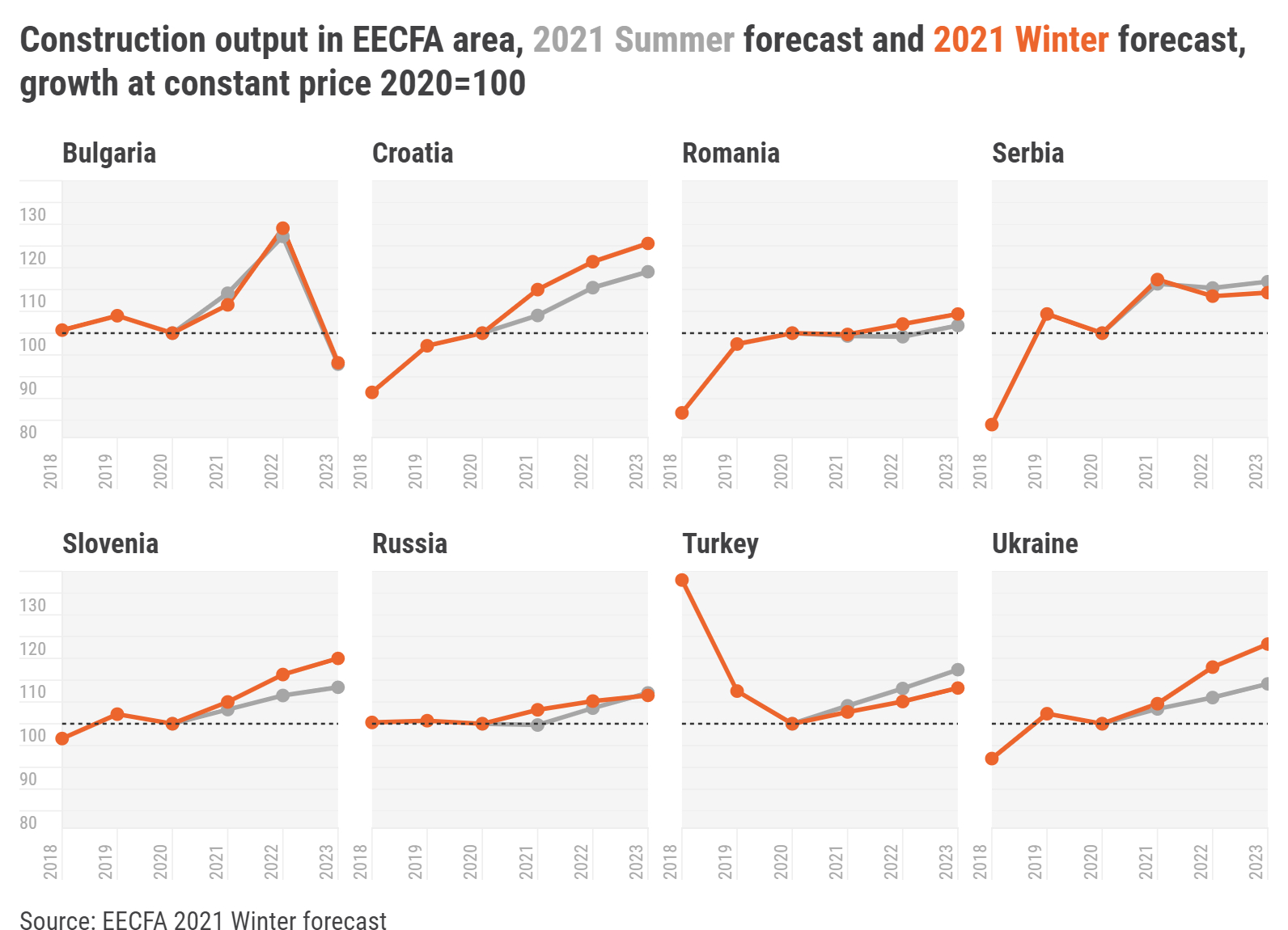

Bulgaria. The Bulgarian economy is recovering more slowly than expected, and the likely growth rate is 3.8% in 2021. However, residential construction looks strong thanks to low interest rates on housing loans, making home purchase more affordable. Real estate is also the safest and easiest way for those wanting to invest to avoid negative deposit rates. The pandemic and its lasting follow-up effects played an additionally strong cooling effect on non-residential construction because of a surge in office and industrial construction earlier and with an emptying pipeline. Zero progress on big-league infrastructure projects will take its toll on growth in civil engineering construction in 2021, but it is set to catch up in 2022. Total construction output in Bulgaria is anticipated to grow by 6.5% in 2021 and 16.5% in 2022. The lack of preparation for the new programming period 2021-2027 and the National Recovery and Resilience Plan are to negatively affect total construction output which is expected to drop by 24.9% in 2023.

Croatia. Croatia’s tourism season surpassed all expectations, driving a 16.2 percentage point swing in the country’s GDP growth, from -8.1% in 2020 to +8.1% this year, and a one-notch jump in its Fitch rating, to BBB. The near-term future of Croatia’s construction sector now depends greatly on the evolution of the COVID-19 pandemic, particularly its effect on tourism. EU and international financial institution crisis-relief funding will, though, soften any blow that the disease delivers. The City of Zagreb’s budget crisis, bureaucratic delays in spending crisis-relief money and much higher construction costs are other negative factors that will affect the growth of construction output, which must be assessed not for the sector as a whole, but segment by segment (e.g., hotels vs. residential).

Romania. The economy is expected to return to pre-pandemic levels, in terms of GDP, by the end of 2021, after growing 7% in real terms. The European Commission forecasts Romania’s GDP growth rate to stay above the EU average in both 2022 (5.1%) and 2023 (5.2%), and, with the help of the Recovery and Resilience Facility (RRF), construction would have a positive ground to grow upon. Total construction output in 2021 is predicted to slightly decline (-0.3%), but to recover and grow in 2022 and 2023. Low interest rates and excess liquidity coalesce into an expanding residential subsector, while non-residential construction continues to be impeded by pandemic-related changes to work habits and various restrictions. On the back of the RRF and the 2014-2020 EU cohesion funds, and despite ongoing difficulties and delays in implementing projects, civil engineering construction continues to have a high potential for growth.

Serbia. After the restrictions in 2020, economic recovery came faster than expected and GDP growth is estimated to reach at least 7.3% in 2021. This strong rebound is supported by accelerated construction activity and increased capital investments, where a high single-digit expansion is projected in 2021 outputs. Construction output is fuelled by civil engineering projects, but also the robust residential and industrial related constructions. Furthermore, budgetary expenditures for investments are planned to reach record levels, with 7.5% of GDP dedicated for this purpose in 2022.

All indicators are pointing towards more extensive growth and sustained construction activity at record levels in this forecast horizon.

Slovenia. The Slovenian economy has rebounded stronger than expected after the pandemic. One of the strongest economic growth accelerators was gross fixed capital investment, causing construction output to get back on feet. Total construction output is projected to exceed EUR 4bln sooner than previously predicted – already in 2022 – and reach EUR 4,3bln in 2023. Construction cost growth will probably slow down from a hike in 2021, resulting in a more stable construction environment without supply shocks. This will enable several big civil engineering projects to continue apace, but the main contributor to construction output will be new residential projects. Of course, our forecasts remain contingent on the condition that no further lockdowns hinder the overall economic activity.

Russia. The construction industry in Russia is going through the second year of the pandemic relatively successfully, and the previously expected stagnation in 2021 is likely to turn into a 3.2% growth by the end of the year. This unexpectedly good result was enabled by segments with traditionally active government participation: residential and civil engineering which were supported by large funds. The non-residential subsector also contributed to the growth of the construction market in 2021, mainly due to the massive completion of objects whose construction was previously postponed from 2020. But because all these factors are temporary, construction market growth in 2022 and 2023 will lessen and is prognosticated to post +1.9% and +1.2% per year, respectively, as a part of the potential for the positive dynamics was already exhausted in 2021.

Turkey. The Turkish economy started to regain senses from the pandemic blow in Q3 2020, which continued with high GDP growth in Q2 2021. Although Turkey removed most COVID-19 related restrictions on 1 June 2020 with the elevated number of vaccinations, now, like across Europe, the fourth wave of the pandemic has started (yet with relatively fewer new cases). The estimated economic growth rate by end 2021 is about 10%, but the primary concern in recent months has been high inflation caused by the national currency’s devaluation. Building starts expanded greatly, but completions registered a small drop in the first 9 months of 2021. The government requires interest rates (also for mortgages) to be kept at less than half of the rate of rise in building construction cost. Keeping real incomes positive during high inflation times is important for demand for commodities like housing and other real estates. Turkey’s total construction output is prognosticated to be positive in the forecast horizon with an average growth of 2.6% up to 2023.

Ukraine. For the construction sector in Ukraine, 2021 marks the year of completion of the construction regulation reform launched back in 2019. In mid-September, the newly created State Inspectorate for Architecture and Urban Planning began to work as a full-fledged new body with its own structure, powers, and new work principles.

Ukraine’s construction market in H2 2021 has showed a good recovery in investment activity and the resumption of construction. The residential subsector remains the driver of the construction sector due to stable demand from the population. The main constraint in the development of the construction market in 2021 has been increased construction costs despite the active implementation of residential projects against the backdrop of the revival of mortgage lending, increased demand from the manufacturing sector, as well as high volumes of financing.

Source of data: EECFA Construction Forecast Report, 2021 Winter

If you would like to receive a sample report please use the following contact button or send an e-mail to sales@proidea.ro.